“Health nuts are going to feel stupid someday, lying in hospitals dying of nothing.”

–Redd Foxx

A health savings account (HSA) is a tax-sheltered account designed to allow you to use tax-advantaged money to pay for healthcare expenses, and if you do not need to use it to pay for healthcare expenses, then you can invest that money in the market, and the money will grow tax-deferred. In order to be eligible to use a HSA, you need to be enrolled in a health insurance program that qualifies as a high deductible healthcare plan (HDHP).

If you’re fortunate enough to be in a situation where you have maxed out your tax-free (Roth) and tax-deferred (traditional IRA/401(k)) retirement savings options, you do have the option of using a health savings account as another tax-deferred retirement option.

HSAs are meant to be used to pay for qualified medical expenses in conjunction with a high deductible healthcare plan. Contributions are deductible on your tax return, even if you don’t itemize, and withdrawals for qualified medical expenses are tax free.

However, if you don’t use up all of the funds in your HSA by the time you turn 65, you can make withdrawals from the HSA account and you are not penalized for withdrawing those funds to spend on something other than qualified medical expenses. The funds are taxed, but you will have gained the benefit of years of tax-deferred growth.

HDHPs are so named because they do have high deductibles before the insurance coverage kicks in. 2020 HDHP deductibles range from $1,400 to $6,900 for singles and between $2,800 and $13,800 for families. The amount you can contribute to a HSA annually is, in 2020, $3,550 for a single person and $7,100 for a family.

Therefore, it’s quite possible for you to have a deductible which is greater than the amount which you contribute to your HSA. It may take a few years before your HSA account has enough in it to cover the deductible with money left over.

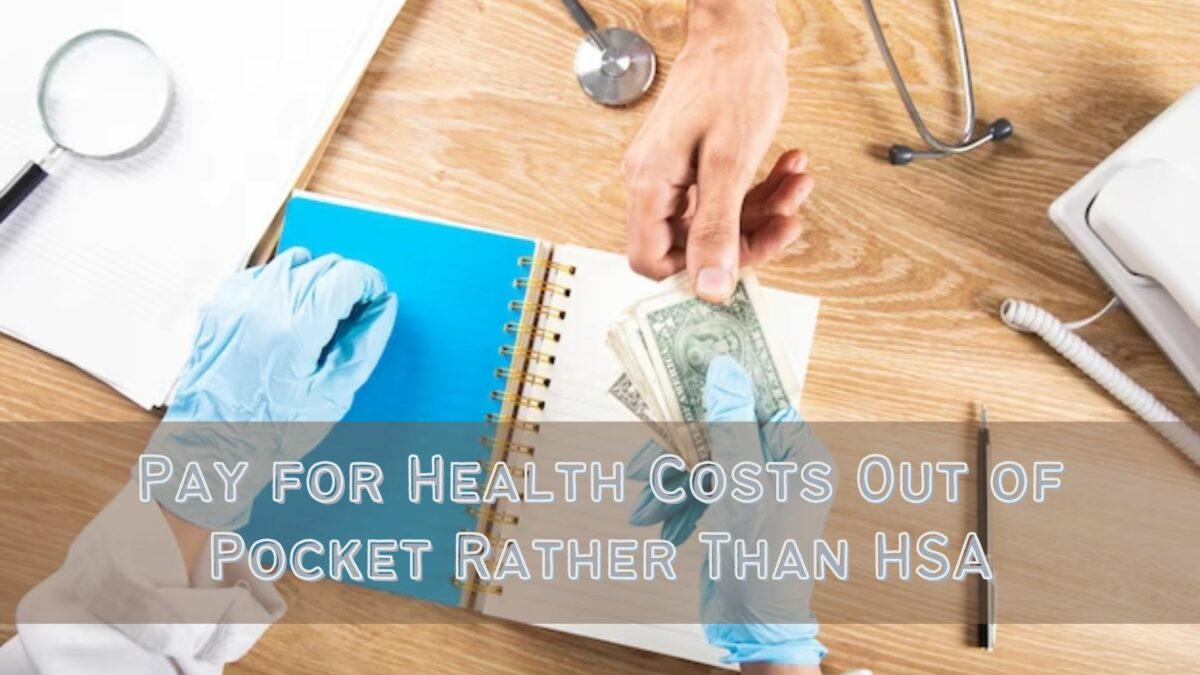

When you have a HDHP with a HSA, you’re not required to pay for your out-of-pocket medical expenses with your HSA funds. You could choose to pay for those expenses with other money, leaving the money in the HSA to continue to grow tax deferred.

If you’re concerned about doing your taxes correctly, I’ve used

TurboTax Online for several years, and, despite the complicated status of our taxes, have had no problems filing my taxes, saving us almost $1,000 compared to what we were paying our accountant when he prepared our taxes.

What are some considerations for determining if you should pay out of pocket versus using your HSA funds?

- You have enough money outside of the HSA account to cover the out of pocket expenses. The best way to get to this point is to set up a separate budgeting bucket for deductible coverage to fund it. That way, you will ensure that you have the money when it’s needed.

- If your expenses will get you above the 7.5% AGI threshold for deducting medical expenses. The savings won’t be large – don’t expect this to put a lot of money back in your pocket. At best, you’ll get back your tax rate * (medical expenses – .075 * AGI).

- If your medical expenses are low. If you don’t spend a lot on medical expenses, then it’s likely that paying out of pocket, particularly if you can afford to fully fund your HSA, won’t set you back much farther.

- If you have the advantage of time for compounding. The tax deferral by a year or two won’t have a significant impact on your retirement funding. Delaying paying the tax by decades will.

- If you have a family history of longevity. While it never makes sense not to prepare for retirement and to reach a ripe old age, having a realistic sense of whether or not you’ll get there should factor into your decision making.

- Your HSA funds are invested in the market rather than in cash instruments. There is no point in deferring taxes on growth if there will never be growth.

- If you are planning on retiring before you can make penalty-free withdrawals from retirement accounts. You will need to save up all of your receipts, but you don’t have to get reimbursed from a HSA at the time that you incur the medical expense. You can get reimbursed at whatever time you choose and not have to pay a penalty, as long as it’s an authorized reimbursable expense. Therefore, if you accumulate several years of medical expenses which you don’t use your HSA to pay for, you can withdraw from the HSA later to reimburse yourself. It may not be much, but what you’ve saved up could account for a year or two in expenses that you could withdraw tax-free.

Using a HSA as a secondary retirement funding option is viable for those who can afford it. If paying out of pocket instead of using your HSA means that you’re going to have to go into debt or sacrifice some of your other goals, then use the HSA for the purpose for which it was intended. However, if you have the funds to afford it, as long as the tax treatment of HSA withdrawals for people 65 and older is favorable, then this is an excellent secondary tax deferral strategy.

Author Profile

- John Davis is a nationally recognized expert on credit reporting, credit scoring, and identity theft. He has written four books about his expertise in the field and has been featured extensively in numerous media outlets such as The Wall Street Journal, The Washington Post, CNN, CBS News, CNBC, Fox Business, and many more. With over 20 years of experience helping consumers understand their credit and identity protection rights, John is passionate about empowering people to take control of their finances. He works with financial institutions to develop consumer-friendly policies that promote financial literacy and responsible borrowing habits.

Latest entries

BlogJuly 8, 2024How to Fast-Track Approval for Section 8 Vouchers

BlogJuly 8, 2024How to Fast-Track Approval for Section 8 Vouchers BlogJuly 8, 2024Unlock Apple Business Credit with No Credit Check Needed

BlogJuly 8, 2024Unlock Apple Business Credit with No Credit Check Needed BlogJuly 8, 2024A $18 Million Per Year Investment Plan for Democrats to Control the Texas House

BlogJuly 8, 2024A $18 Million Per Year Investment Plan for Democrats to Control the Texas House Low Income GrantsSeptember 25, 2023How to Get a Free Government Phone: A Step-by-Step Guide

Low Income GrantsSeptember 25, 2023How to Get a Free Government Phone: A Step-by-Step Guide