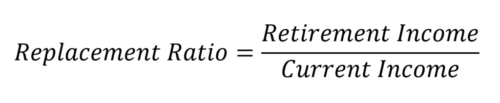

When talking about retirement, most financial planners use a wage replacement ratio (WRR) to estimate whether or not you’re going to have enough money to retire. The approach is a top-down approach to figuring out how much you’ll need in retirement by taking a percentage of what you make in the year before your retirement.

The approach is wrong. How so? As long as you don’t live on the hedonic treadmill, then the amount of income you make does not affect your expenses. Thus, the approach to figuring out how much you need in retirement should be to figure out how much you’re going to spend in retirement and determine if your assets can support that spending going forward. You’ll have to account for taxes: dividend income, capital gains, income taxes on pensions and the like, Roth conversions if they are available, and, as appropriate, tax due from tax-deferred retirement accounts. The amount withdrawn pre-tax should be below a safe withdrawal threshold and the after-tax funds should be enough to pay for your expenses.

If you’re there, then you can retire.

If not, there are a couple of things you can do.

- The simple answer: keep working. Working is what brings in income to both cover current expenses and to provide more investable capital to grow the retirement nest egg.

- The harder answer: evaluate your expenses and see if there are ways to cut your spending without affecting the quality of your life. If you can cut expenses and still have a happy life, then you’re a potential candidate for retirement. However, if not, then you need to weigh whether working to beef up your reserves outweighs your desire to retire.

Figuring out whether you can retire, particularly if you don’t have an inflation-adjusted pension that exceeds your expenses, is always going to be somewhat of a crapshoot. Rules of thumb, such as a 4% safe withdrawal rate, are just that – guidelines. Short of having assets like Bill Gates and spending habits like Silas Marner, at some point, the decision of whether or not you can retire on what you have becomes an educated guess.

It’s important to know where you are, where you’re going, and what’s important to you in your financial journey. Even if you’re young, having an idea of where you need to be and what’s meaningful to you in your life will help guide your decisions both now and down the road. Understanding your spending both now and in the future will give you an idea of what assets you’ll need to save, but simply plugging in a formula for replacing your income fails to take into account where that money goes and how much is needed. It’s critical to analyze, instead, how much money you’ll need for spending and work from there.

Author Profile

- John Davis is a nationally recognized expert on credit reporting, credit scoring, and identity theft. He has written four books about his expertise in the field and has been featured extensively in numerous media outlets such as The Wall Street Journal, The Washington Post, CNN, CBS News, CNBC, Fox Business, and many more. With over 20 years of experience helping consumers understand their credit and identity protection rights, John is passionate about empowering people to take control of their finances. He works with financial institutions to develop consumer-friendly policies that promote financial literacy and responsible borrowing habits.

Latest entries

BlogJuly 8, 2024How to Fast-Track Approval for Section 8 Vouchers

BlogJuly 8, 2024How to Fast-Track Approval for Section 8 Vouchers BlogJuly 8, 2024Unlock Apple Business Credit with No Credit Check Needed

BlogJuly 8, 2024Unlock Apple Business Credit with No Credit Check Needed BlogJuly 8, 2024A $18 Million Per Year Investment Plan for Democrats to Control the Texas House

BlogJuly 8, 2024A $18 Million Per Year Investment Plan for Democrats to Control the Texas House Low Income GrantsSeptember 25, 2023How to Get a Free Government Phone: A Step-by-Step Guide

Low Income GrantsSeptember 25, 2023How to Get a Free Government Phone: A Step-by-Step Guide