Today the number of international transactions has skyrocketed with an average turnover of US $574 in 2016. High international transfer costs and high vulnerability are important reasons for shifting from traditional banks to online transfers. Various FinTech companies offer similar benefits, but not all of them are highly successful.

Most of the successful companies in this industry use Blockchain technology to transfer money. Blockchain technology is not only limited to money transfer agencies but also has entered into the finance industry, and most of the big international banks are incorporating Blockchain into their money transfer. Today, in this article, we will cover in-depth information about Blockchain technology and how ICICI bank, one of the biggest banks, has incorporated Blockchain technology in their money transfer process.

How ICICI Bank Shaped the Indian Economy with Blockchain?

The partnership of Steller, one of the biggest non-profit Blockchain platforms, with one of the biggest banks in India, ICICI bank, was truly remarkable and had a great impact on the Indian economy. It was very important and in demand for India to shift to cash-free transfers and introduce money wallets during the time of cash freeze or demonetization when it became practically impossible to pull out cash from the ATM, and all the day-to-day transactions were halted.

Furthermore, the same has been seen in the Philippines, and Africa saw a steep growth of cryptocurrencies. Africa board fellows deliberate also have shown declining in bank transfers and more online transfers in Banks. Around that time, bank wallets introduced in partnership with Steller saw heavy users among university students and office-going individuals, which made their life extremely easy and stress-free. This was a revolutionary movement that shaped the Indian Economy and tamped the banking structure in such a developing country with millions of people.

What is Blockchain Technology?

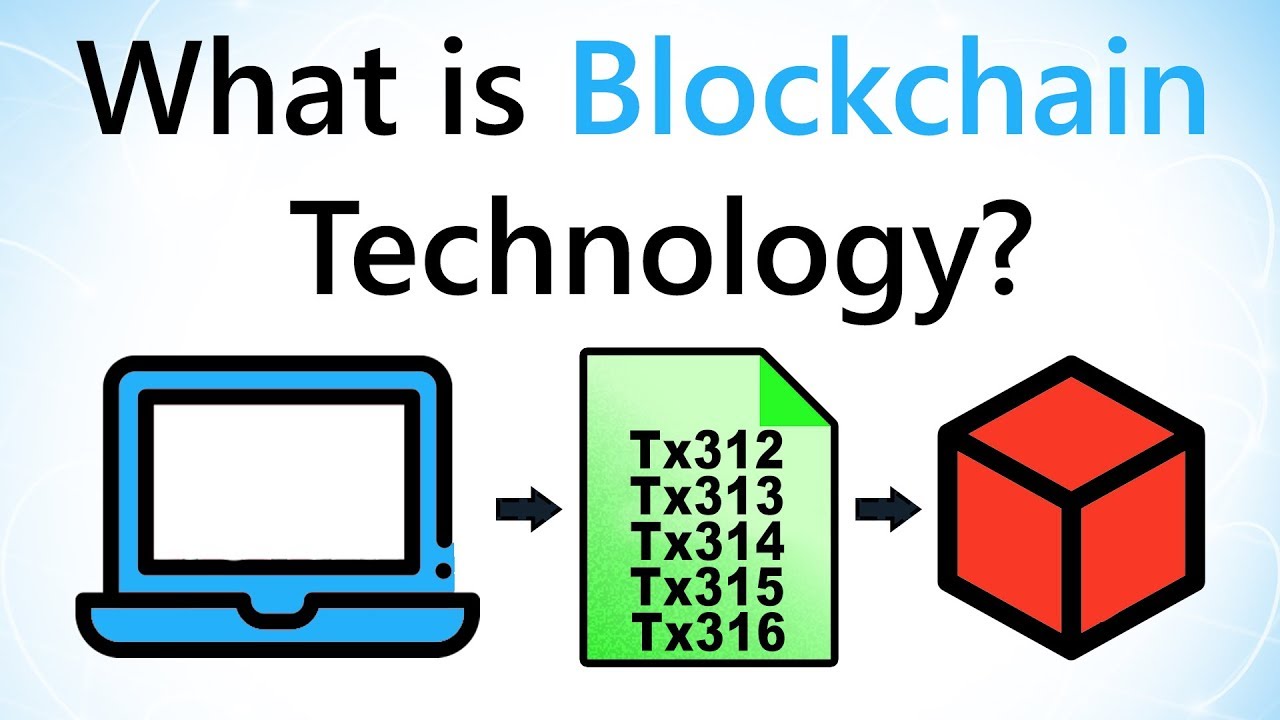

A Blockchain is a technology that provides peer-to-peer networking through various servers or computers, which are known as ”nodes” which let you monitor the transactions of various information and benefits. On every system or node, all the daily transactions are recorded, creating a trust-based platform providing a certain unique duplicate of the archives.

It is a groundbreaking technology that enables us to share information and cryptocurrencies. One of the most helpful things about Blockchain is that no third party is involved in the process, which certainly increases efficiency, safety, and trustworthiness in various sectors. Blockchain technology has been used in various sectors, starting from agriculture to businesses and banks. It has a great impact on economic stability, marketing, and business deals for a number of sectors.

The History of Blockchain

Blockchain Technology was first released in 2008 by a person going by the name “Satoshi Nakamoto”. He used a Hashcash-like strategy and successfully upgraded the structure of the Blockchain, which keeps track of the date and timings of the transactions and adds blocks by keeping certain boundaries and without involving any third party in order to balance the rate at which the blocks were added.

By the end of one year, It was considered one of the important parts of cryptocurrency to carry out all the transactions and keep a real-time record of the money transferred. The size of the stored data started to increase in 2014, which witnessed the size of the record exchange standing at 20GB, and the next year it went up to 30 GB. And it reached 200 Gib by mid-2020. This market size is expected to grow more in the near future.

How Does Blockchain Work?

Blockchain technology has a mechanism where it utilizes hash functions and distributed ledger, then it converts the transaction to a particular code, which is then shared and goes through several processes of checking. It is sometimes difficult to find every algorithm that creates a hash, so a hash uses a particular code made of numbers to find out any sort of necessary information. Several inbuilt features make hash very hard to crack by any hackers and thus very difficult to hack the system.

After this step, the hash is carefully incorporated into the Blockchain. To prevent confusion, every copied block of hash is matched with the previous entry. Though it is quite impossible to change the structure of a hash, still, if someone wants to change it, they have to change the whole structure. The sequence of the blocks changes after every 10 minutes. Within this particular time, it is totally unfeasible to hack the system.

How Blockchain Helps in Money Transfers?

- One of the most important advantages of Blockchain is that it doesn’t require any middleman or third party to transfer crypto or money from one wallet to another wallet. The money here is transferred directly between the receiver and the sender.

- With Blockchain technology, merchants now do not need to worry about the banks giving refunds against their money. There is a high chance of final transactions without any failure.

- It offers a very smooth and easy procedure to transfer money, all you need to do is give your receiver’s address, and phone number and the funds will be instantly transferred into their wallet.

- Blockchain has a very efficient and reliable money transfer procedure because in various countries with low banking facilities and a lack of proper networking leads to various failed payments. Sometimes, it is also observed that the amount is deducted without making the actual problems. And there are no definite solutions which are provided to overcome this issue. Blockchain technology enables a very reliable transfer of funds with fewer fees.

The Different Types of Blockchain Technology

There are four types of Blockchain Technology available, which are as follows:

- Public Blockchain

- Private Blockchain

- Hybrid Blockchain

- Consortium Blockchain

1. Public Blockchain

This is the type of Blockchain that is open to anyone and everyone who wants to join. It does not have a central authority to invigilate. Anyone with any network can join the Blockchain. All you need to have is a stable internet connection to sign in to the network. It has features that enable users to monitor past records, confirm transactions, and fix bugs.

However, for security reasons, it is not possible to change any data on your own; you can always suggest improvements. Most contemporary cryptocurrencies run on public-domain Blockchains. Public networks are not controlled by a single user.

Pros

- This is not controlled by any single user and hence is open to all.

- They follow complete transparency in their transaction.

- It is completely global.

Cons

- Does not have high transaction speed.

- The transaction fee is high.

2. Private Blockchain

These Blockchain networks are owned by private organizations and are not open to everyone. Joining a private Blockchain network requires an internet connection but, more importantly, permission from its managing authority. Organizations use it mostly to monitor organizational activity, like deleting and recommencing data. They provide safety to an institution or organization’s data by keeping it highly secure.

Private Blockchains have relatively higher speeds than public Blockchains due to their lower number of users, but they are not totally decentralized, as users claim they have their own controlled authority.

Pros

- Have high transaction speed.

- Relatively lower energy usage.

- It can be scaled.

Cons

- It is not secure and trustworthy.

- Not totally decentralized.

3. Hybrid Blockchain

Hybrid Blockchains are a mixture of private and public Blockchains. The positive aspects of both public and private Blockchains are held within this Blockchain. Through this Blockchain, selected portions of data can be made public while the majority remains private.

Although a greater power controls this Blockchain, it also occasionally grants freedom. The authority may choose to make any transaction public or private as they see fit. Despite that, that power never changes once a transaction is validated and a block is added to the Blockchain. A hybrid Blockchain is, therefore, secure and decentralized at the same time.

Pros

- Its ecosystem is incredibly adaptable.

- It operates at a very rapid pace.

- This is safe.

Cons

- Does not maintain transparency.

- It is very frantic to maintain.

4. Consortium Blockchain Network

A consortium is an alliance of several organizations. Hence, a consortium Blockchain is a type of Blockchain where various organizations come together to form a federated Blockchain. It is managed by a number of organizations rather than just one and is more decentralized than a private Blockchain. Yet, it is a private Blockchain with permissions.

Pros

- It is protected against threats like SQL injection.

- It is adaptable.

- Economically sound.

Cons

- It is difficult to upgrade the protocol in this case.

- In this Blockchain, there’s an apparent lack of collaboration.

Is Blockchain Network Secure?

- A Blockchain system may appear to violate one’s privacy, but it helped build trust and grow digital financial services.

- A Blockchain money transfer can be seen by all involved parties due to its public nature, which offers an encrypted and unchangeable basis of trust.

- The security of the Blockchain is one of its main advantages. Blockchains essentially cannot be hacked and encrypted. Users will gain from this, but regulators will be concerned. The data model of a Blockchain cannot be changed or removed.

- To change the structure of the nodes, one needs to alter the whole structure of the nodes, which is practically impossible as the data structure is altered within just ten minutes.

- Blockchain technology adds an additional layer of protection for local business payments in light of previous financial scandals and economic meltdowns. Small firms might benefit most from using Blockchain technology to protect their money.

- Faith frequently loses business money, and bankers and governmental organizations profit from this reality. Blockchain completely eliminates the need for it. Businesses must spend a lot of money and years establishing trust. Yet, users of Blockchain have the advantage of renunciation faith in both governments and business partners.

Drawbacks of Blockchain Money Transfer

- Blockchain technology is not free, despite the fact that it can help consumers save money on transaction costs. For instance, the PoW mechanism used by the bitcoin network to verify transactions demands a tremendous amount of processing power. Users continue to run up their electricity costs to verify the integrity of Blockchain transactions despite the costs associated with mining bitcoin. This is due to the fact that miners are compensated with enough bitcoin for their time and effort when they add a piece to the Bitcoin Blockchain. To validate transactions on Blockchains that do not employ cryptocurrencies, nevertheless, workers must be paid or given some other incentive.

- While secrecy on the public Blockchain safeguards users’ privacy and prevents hacks, it also enables illicit activities and trade on the network. With Web Browsers and the dark web, users can purchase illicit things using cryptocurrencies such as Bitcoin and sell them without being seen. Banking service providers are obligated by current U.S. rules to collect information about their clients whenever they open an account, validate each client’s identity, and ensure that they do not appear on any lists of recognized or believed terrorist organizations. This approach has both benefits and drawbacks. Everyone can access financial accounts, but it also makes it simpler for thieves to conduct transactions. Several have claimed that the positive uses of cryptocurrencies, such as banking the unbanked globe, outweigh the negative uses, particularly as the majority of unlawful conduct is still carried out using untraceable cash.

- Concerns pertaining to governmental regulation of cryptocurrencies have been raised by a lot of the crypto community. Governments might conceivably make it unlawful to hold cryptocurrencies or take part in their networks, even though it is getting more and harder to stop some kind of Bitcoin as its decentralized network grows.

- One of the major negatives is the scalability issue, which can be problematic for any person or corporation. Scalability is the explanation. If there is a lot of network traffic during a transaction, the operation won’t be able to be finished. Due to the fact that so many investors conduct business using this technology, it is one of the greater and more important problems. Also, we are aware that the network slows down during traffic jams because there are so many investors in bitcoin cryptocurrency. When scalability problems are severe enough, transactions might take days or even weeks to complete.

Frequently Asked Questions (FAQs)

Q1. Which banks are using Blockchain technology in India?

Banks that are using Blockchain technology in India are as follows: ICICI Bank, IndusInd Bank, IDFC Bank, Yes Bank, South Indian Bank, RBL Bank, and Federal Bank.

Q2. Does ICICI Bank use Blockchain?

Yes, ICICI Bank, in partnership with Steller, is one of the biggest banks in India that uses Blockchain for money transfers. Around 1994, they also followed the traditional banking style of standing in long queues, but they shifted towards bank wallets during the time of demonetization in India, which was a very big step towards digitalization in India.

Q3. Will Blockchain replace banks?

The simple answer is that yes, banks and traditional financial systems can be replaced with decentralized finance (DeFi). Cash might be easily replaced by cryptocurrencies as a way of conducting barter exchange, a store of value, and a unit of account.

Q4. What is the future of Blockchain in the banking industry?

This is especially helpful when accurate and tamper-proof transaction records are required. Blockchains can be used, for instance, to track and settle deals, manage financial assets, handle payment processing, and even design safe smart contracts between various parties. It has a great future in the banking sector as there is a great possibility that traditional financial systems will be replaced by DeFi in the near future.

Bottom Line

Blockchain Technology is one of the most frequently debated topics of this era. The technological advancements helped in accelerating financial inclusion with new data, and more knowledge about Bitcoin and Cryptocurrency has made this technology more popular and feasible to every investor in the country. It is a great way to provide seamless, easy transfer of money in developing countries where the banking and financial systems are not developed.

But, there are various downsides that come with this technology, like scalability, illegal payments, and high power consumption. Still, it is estimated to grow its market in the near future as most of the traditional banks will be replaced by most of the DeFis.

Author Profile

- Jonas Taylor is a financial expert and experienced writer with a focus on finance news, accounting software, and related topics. He has a talent for explaining complex financial concepts in an accessible way and has published high-quality content in various publications. He is dedicated to delivering valuable information to readers, staying up-to-date with financial news and trends, and sharing his expertise with others.

Latest entries

BlogJuly 8, 2024Introduction to Tax Liens and Deeds

BlogJuly 8, 2024Introduction to Tax Liens and Deeds BlogOctober 30, 2023Exposing the Money Myth: Financing Real Estate Deals

BlogOctober 30, 2023Exposing the Money Myth: Financing Real Estate Deals BlogOctober 30, 2023Real Estate Success: Motivation

BlogOctober 30, 2023Real Estate Success: Motivation BlogOctober 28, 2023The Santa Claus Rally

BlogOctober 28, 2023The Santa Claus Rally