“When I’m bearish and I sell a stock, each sale must be at a lower level than the previous sale. When I am buying, the reverse is true. I must buy on a rising scale. I don’t buy long stocks on a scale down, I buy on a scale up.”

–Jesse Livermore

When investing in Value Cost Averaging or Dollar Cost Averaging, people often fear that they’re going to miss the great run-up or miss the next great buying opportunity. We tend to overreact when we see a stock going up and think that we’re going to miss the next great Google, Apple, or Pets.com and rush to buy. On the other side, when stocks are sliding, we tend to panic and think that they can only go down. As a result, individual investors often buy high and sell low – the polar opposite of what they want to do.

A common way that people pose for avoiding this scenario is to invest the same amount periodically, called dollar cost averaging. So, let’s say that you want to invest $1,500 in a year. Instead of buying all at once, invest $125 per month. That will ensure that you buy more when the price is lower and less when the price is higher. In general, this is a better approach than the buy-all-at-once approach. Naturally, if you buy at the lowest price in a year, you can do better, but how many of us are so skilled at market timing that we can do that?

What dollar cost averaging doesn’t accomplish is allowing you to spend more when prices are lower and spend less (or even sell) when prices are higher. This approach is called value cost averaging or, sometimes dollar value averaging. The approach to value cost averaging is to specify a given return on money invested and then buy or sell shares to get to that total value. So, let’s say that you want to invest $1,500 in a year and want an 8% return. The first year, you invest $1,500. In the second year, that $1,500 should be worth $1,620, and you’ll add another $1,500. Therefore, you buy or sell enough shares to have a total of $3,120 worth of shares.

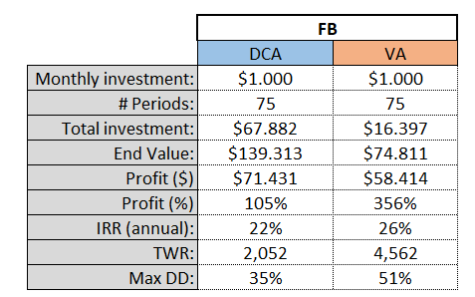

How does value cost averaging work compared to dollar cost averaging? Furthermore, how often should you do this?

I did an analysis of three commonly held USAA funds for doing this calculation. I looked at USSPX, USMIX, and USAGX. Two are broad market indices, while USAGX is their gold and precious minerals fund. I also assumed buy or sell orders went in after the market close, since, for value cost averaging, it is impossible to know how much to buy in a given day to put in the order before the market closes; therefore, I used the previous day’s close for pricing. Furthermore, I assumed reinvestment of dividends and capital gains and so used the adjusted closing price to normalize.

For dollar cost averaging, I assumed a purchase on the first available trading day in a period. For daily, this was not necessary, as purchases were made every day. I did the same for value cost averaging and then calculated the periodic return based on an 8% annual return – which is a different calculation than simply dividing by the number of periods. I started at each fund’s inception and ran the calculations through June 11, 2012.

Investment timing is everything and a variable you cannot here control. – Click to Tweet

Since the minimum incremental investment for each of these funds is $50, which, by the way, is not the same amount required to start an investment in the fund, that is the daily increment I used. I added $50 to the “investment kitty” every trading day to keep the amounts the same for daily, monthly, or annual investing.

The results were very clear. In every instance, daily value cost averaging was the best way to invest. Then, monthly value cost averaging was second best. The results differed for the USAGX fund, as annual dollar value averaging was the worst investment strategy; however, for the other funds, it was the third best. This seems to be because the fund suffered a precipitous drop from the beginning of 2012, meaning that the last purchase, which was much larger in value cost averaging than in dollar cost averaging, bought a lot of shares that aren’t worth as much as now.

Similarly, increased frequency of investing improved dollar cost averaging, with annual dollar cost averaging returning the lowest returns.

What conclusions can we draw from this evaluation?

- If you’re willing to do it, daily value-cost averaging is the best way to go. If I managed a large, large amount of money for someone, this is the way I would go.

- Daily value cost averaging means that you’re going to be doing calculations and making purchase orders every day. The reason that daily value cost averaging does the best is that you’re forced to buy and sell at every movement. Whenever you increase the periodicity of your investments, you’re going to miss out on some swings because you’re averaging performance over time.

- Monthly value cost investing seems to be the best balance between time commitment and returns. This should be an exercise that takes 10 minutes every month.

- Value cost averaging works not only because you are buying low and selling high relative to your returns, but also because it is, in effect, a forced savings program. If your investments aren’t returning your expected return, then you are forced to put more money in. This means, in all likelihood, that you are forcing yourself to invest more when the market is down.

- You may have to invest more than you expect, particularly in the beginning, if you value the cost average. Since the idea is to invest more money when the market is down, you may have to draw some more from your cash reserves than you might expect to. Eventually, assuming an inevitable rise in the market, you will be selling some shares which will then provide cash reserves to make subsequent purchases.

- Timing is still everything and a variable that you cannot control. If you retire just as the market begins to tank, you’re going to have to lower your withdrawals. However, if you start investing right at the end of a very large market decline and at the beginning of an upturn, your results will look great. You could take the same investing approach in two different time periods and wind up with vastly different results simply because of when you started investing and when you retired.

- Your results may vary, and past performance doesn’t indicate future results. You already know this, but I can’t guarantee that the future will mimic the past. It’s like walking up to a roulette wheel that has landed on black fifteen straight times and betting on red, thinking “It can’t be black again!”

Granted, the analysis I did was on the back of a grand total of three mutual funds. In order to really draw conclusions, it will be necessary to analyze many more funds to get some semblance of statistical significance. Still, given the results I’ve seen, I think it’s reasonable to draw preliminary conclusions about the effectiveness of value cost averaging compared to dollar cost averaging and the conclusions of the effectiveness of investing as often as possible rather than only investing annually.

Author Profile

- John Davis is a nationally recognized expert on credit reporting, credit scoring, and identity theft. He has written four books about his expertise in the field and has been featured extensively in numerous media outlets such as The Wall Street Journal, The Washington Post, CNN, CBS News, CNBC, Fox Business, and many more. With over 20 years of experience helping consumers understand their credit and identity protection rights, John is passionate about empowering people to take control of their finances. He works with financial institutions to develop consumer-friendly policies that promote financial literacy and responsible borrowing habits.

Latest entries

BlogJuly 8, 2024How to Fast-Track Approval for Section 8 Vouchers

BlogJuly 8, 2024How to Fast-Track Approval for Section 8 Vouchers BlogJuly 8, 2024Unlock Apple Business Credit with No Credit Check Needed

BlogJuly 8, 2024Unlock Apple Business Credit with No Credit Check Needed BlogJuly 8, 2024A $18 Million Per Year Investment Plan for Democrats to Control the Texas House

BlogJuly 8, 2024A $18 Million Per Year Investment Plan for Democrats to Control the Texas House Low Income GrantsSeptember 25, 2023How to Get a Free Government Phone: A Step-by-Step Guide

Low Income GrantsSeptember 25, 2023How to Get a Free Government Phone: A Step-by-Step Guide