“Coward: One who, in a perilous emergency, thinks with his legs.”

–Ambrose Bierce

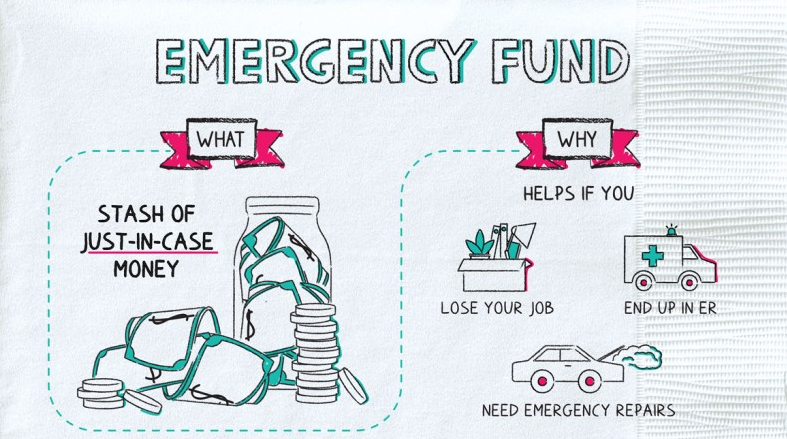

Six months of savings in an emergency fund…

You hear that nugget of wisdom all of the time. It’s usually followed by:

“…kept highly liquid like a money market account.”

Is that thinking right?

We’ll explore that question in today’s article along with some research that may surprise you.

First, though, let’s explore the whole notion of why we might have an emergency fund in the first place.

Do you think Bill Gates has an Emergency Fund?

Think about this for a second.

Your answer is probably the same as everyone else’s.

Of course not!

When he needs a new roof or has to buy braces for his kid, he simply instructs his butler to stroke a check. Or, if his yacht sank and he needs a new one, he calls his broker and liquidates a few hundred thousand shares of Microsoft to pay for it.

There is no such thing as a financial emergency for the wealthy. They simply write checks for their bills (or have their personal assistants do so), and they continue on.

They have sufficient assets to pay for whatever might come along, and they are not dependent on a job to provide them with income.

Compare that with a twentysomething who is looking for financial security from two possible major events:

- Loss of a job, requiring spending savings to live on while waiting for another job.

- An expense that costs more than the person has saved up in assets outside of a retirement account that can’t be accessed without paying significant penalties.

When one of those occurs, the person usually has Sophie’s choice of either taking money out of retirement accounts and paying the early withdrawal penalty (unless medical hardship applies) or racking up credit card debt.

Thus, we hear the advice to keep an emergency fund of six months of expenses so that we can weather any storm that the world may bring.

We use mental accounting to prevent ourselves from going on a wild bender in Vegas with that money.

MONKEY BRAIN: “OOH! LOTS OF MONEY. NEED MAN CAVE…”

YOU: “No touch! Bad Monkey Brain!”

Monkey Brain, what I call our limbic system, will spend any money he can see. He can be fooled into not spending money through the use of what is called mental accounting. Mental accounting is where we create separate categories for our money even though it’s all money. Money from different accounts spends just the same as any other money. However, if we label a certain kind or amount of money “emergency fund,” then suddenly, we’ve created a much higher bar for Monkey Brain to leap over to spend it, and it truly will require something bigger for Monkey Brain to feel comfortable whipping out the wallet.

But, the emergency fund plays on another part of Monkey Brain’s psyche. It plays on an aspect called loss aversion.

When it comes to our emergency fund, we fear that we’ll have saved up six months of expenses, and if we invest that money in the stock market, the market will tank by 50% right when the emergency hits, and boy, will we be sorry THAT happened!

Thus, to prevent ourselves from ever realizing the imagined fear of having to kick ourselves for investing our emergency fund in the stock market, we avoid that loss in the first place by putting the money in the safest places we can think of savings accounts, money markets, CDs, and checking accounts, where they earn, effectively, 0%.

Are we creating an emergency by not investing our emergency funds?

This is the question that a team led by Texas Tech’s Dr. John Gilliam looked to answer.

Before I get into their findings, let me dispel one of the notions regarding emergency funds: liquidity.

The idea behind having a liquid emergency fund is to prevent you from needing to go into credit card debt in extreme cases where you need that money. However, short of being held for ransom in some Third World country, I can’t imagine a situation where you’d need six months of expenses in cash right away. You can sell off liquid investments and then spend the money, and, in an extreme case, you could put the expense on a credit card and then sell the investments to pay off the credit card. You have a grace period with your credit card, so you won’t accrue interest.

Therefore, real estate, fine art, antiques, and gold bars aren’t appropriate investments for what’s allocated as emergency fund money because you can’t get rid of those quickly enough to pay the expenses you might accrue.

Now, onto the findings.

The study examined situations where a person would experience a financial emergency and need to tap into savings or investments to pay for the emergency. The probability of a “financial emergency” was the same as the unemployment rate.

The authors wanted to answer two questions:

- Would having a separate emergency fund in cash affect the amount of money a person had at age 65?

- Would not having a separate emergency fund in cash affect the chances of having sufficient money in the event of an emergency?

The answers were clear in both cases.

How much does an All-Cash Emergency Fund Cost you at Retirement?

The study conducted simulations using stock market and bond market returns and unemployment rates.

After the simulations, the only time that the emergency fund approach was correct was when the person was invested 100% in Treasuries, and it won by 1.89%. At higher equity allocations, investing all of the money was the better approach.

Given that the study evaluated a hypothetical person from age 25 through 65 and that the rule of thumb for investing in stocks is 110 – age, that person, on average, would be invested 65% in stocks and 35% in bonds. The mean improvement over an all-cash emergency fund for investing that money was 19.7%.

Yes, having more in retirement is nice, but, what if you have an emergency and don’t have the money in the first place? What if the market dropped right before the emergency? You’ll regret that decision, won’t you?

Does Investing Emergency Fund Money Affect the Chances you won’t have Enough if you Do have an Emergency?

Keeping your emergency fund in cash is designed to protect you against the worst-case scenario – you have an emergency right after a major drop in the market.

What that thinking doesn’t acknowledge is that for a vast majority of the time that emergency fund is going to grow, thereby increasing the chances that you’ll have enough money to cover an emergency.

The authors looked at having two, four, and six months of emergency funds saved and a range of investment strategies from 0% stocks to 100% stocks.

In every scenario, investing an emergency fund increased the probability of having enough money to cover an emergency.

Since the hypothetical person, on average, will be invested 65% in stocks, I looked at the outcomes for the 60% stock investment bracket from the study.

The more you have saved up in your emergency fund, the more opportunity cost you’re paying by having that money sit in an account that earns nothing for you. For people who have six months of expenses saved up – the standard financial planning target – they’re 35.2% less likely to have sufficient money to withstand an emergency in the event that one happens.

Here’s why investing your emergency fund works.

Investing your Emergency Fund when you’re Young

The amount of money that you’re going to have saved up is relatively small. It may represent a significant portion of your net worth, but it does not represent a significant amount compared to how much you’re going to earn in your lifetime.

As we saw in “Do You Need to Save Money in Your Twenties?” having saved up $83,600 by age 30 was the springboard to retirement success at age 65. You could try to get there just by saving a higher percentage of your salary, but it’s almost certainly easier to get there by letting the markets do some of the work for you.

But, if you do have an emergency that requires tapping into the fund, you have time to recover and can save a little more each month to get back to where you were and, hopefully, exceed it because you’ve established the habit of saving more.

There is one mandatory item to make this work: disability insurance. When you’re young, you can afford to invest your emergency fund in the markets because you have a lifetime of wages to cushion you against any loss. If you become disabled and can’t work, that changes everything. If you’re not protected against that possibility, the results can be disastrous. Scraping by on SSI when you’re disabled is not the place you want to be.

Investing your Emergency Fund When you’re Older

The reasoning for investing your emergency fund when you’re older flips around. Now, the emergency fund is a relatively small percentage of your overall net worth. If you have a million dollars and you need $25,000 to pay for an emergency, you can simply sell assets to pay for that emergency, and it won’t have much of an effect one way or the other. Ideally, if you need to sell the assets from a taxable account, you’ll sell the assets that will be capital losses so that you can offset capital gains. When you have enough in assets that a market drop won’t affect your ability to meet the six months of expenses criterion, then you don’t need to have that money set aside in an account that earns zero interest.

Furthermore, if you have your emergency fund in an account that earns no interest, the number of months of expenses that the fund will cover will decrease over time due to inflation. You want your emergency fund to be robust so that it can continue to cover the unforeseen circumstances of life and not leave you short.

Again, there is one key factor to making this plan work if you’re older. You must have access to the money without paying a penalty from the IRS. If you’re under 55, this means you need to either have a Roth IRA with sufficient contributions to cover emergency expenses – since you can withdraw contributions tax and penalty free at any time – or the have funds invested in a taxable account.

Why I Recommend a Roth IRA for Emergency Funds

Roth IRAs can serve double duty for you. First off, they provide a tax-free retirement account when you reach age 59 ½. Having taxable, tax-deferred, and tax-free money in retirement is key to a successful and lower tax withdrawal strategy. The second benefit is that, if you need to, you can withdraw the contributions tax and penalty-free at any point.

Thus, if you have an emergency, you can access the money. If you don’t have an emergency, then those funds will stay invested in the market and should grow over time, helping you meet your retirement goals.

You want to prepare for an emergency, but remember that it’s unlikely to happen. As we saw in “Monkey Brain Confuses Rates and Raw Numbers,” Monkey Brain takes low-probability events and acts as if they’re going to happen tomorrow. It’s why, when you feel turbulence, you think that the plane is going to go down and you pull out the mental DVD of your life to replay when the reality is that only about 1 in 100,000 planes crash.

If you revolve your financial life around things that probably won’t happen, then you’re going to put an unnecessary anchor around your ankle. It’s OK to take risks. Very few things in life are absolutely irrecoverable, and chances are that none of them will ever happen to you. Plus, as we saw in the research, in this case, the “risky” option is actually safer than the “safe” option.

Where’s your emergency fund? Did this change your mind? Let’s talk about it in the comments below!

Author Profile

- John Davis is a nationally recognized expert on credit reporting, credit scoring, and identity theft. He has written four books about his expertise in the field and has been featured extensively in numerous media outlets such as The Wall Street Journal, The Washington Post, CNN, CBS News, CNBC, Fox Business, and many more. With over 20 years of experience helping consumers understand their credit and identity protection rights, John is passionate about empowering people to take control of their finances. He works with financial institutions to develop consumer-friendly policies that promote financial literacy and responsible borrowing habits.

Latest entries

BlogJuly 8, 2024How to Fast-Track Approval for Section 8 Vouchers

BlogJuly 8, 2024How to Fast-Track Approval for Section 8 Vouchers BlogJuly 8, 2024Unlock Apple Business Credit with No Credit Check Needed

BlogJuly 8, 2024Unlock Apple Business Credit with No Credit Check Needed BlogJuly 8, 2024A $18 Million Per Year Investment Plan for Democrats to Control the Texas House

BlogJuly 8, 2024A $18 Million Per Year Investment Plan for Democrats to Control the Texas House Low Income GrantsSeptember 25, 2023How to Get a Free Government Phone: A Step-by-Step Guide

Low Income GrantsSeptember 25, 2023How to Get a Free Government Phone: A Step-by-Step Guide